Commentary by Banor

MARKET OUTLOOK 2025 – First Half 2025

2024 was a remarkable year for the American stock market. It greatly outpaced the more modest rise in Europe, while in Far Eastern markets, China had a sort of a false start, with the rest of Emerging Markets standing still.

- US Market: the S&P 500 gained 25%, mainly due to multiple expansion – attributable to strong global flows directed towards the stock market – rather than earnings growth. With valuations and sentiment at the highest levels of the world’s main stock exchange, a cautious approach may be warranted for 2025, “Magnificent 7” aside.

- European Market: since the war in Ukraine broke out, there has been a continuous outflow of money from the stock market to the bond market, with valuations discounted by 50% compared to the US stock market. Europe is in a particularly critical but hopefully temporary position: it must become more competitive by pushing the creation of champions in digital technology and energy transition, and strengthening in more traditional sectors, by mobilising large sums of money that only a single capital market can guarantee.

- China: Global investors are very cautious about investing in the Asian giant’s stock market, but despite this, Chinese companies are increasingly competitive both in the domestic market and in foreign markets, with strong signals of support from the government. We believe a position, albeit moderate, in the Chinese stock market should be built with a medium-term perspective.

- Bond Market: monetary policy, after two years, has finally reached its objective: stabilising the inflation rate and paving the way for a gradual rate decrease, albeit with a growing disconnect between Europe and the United States, given that the ECB might cut rates more frequently than the Fed. The credit market continues to outperform government securities. Among the factors underlying the reduction of spreads between corporate bonds and government securities is the underperformance of government bonds. Moreover, corporates will benefit from the support of an expansionary monetary policy and a macroeconomic context that, although disappointing in Europe, should not lead to a recession. Greater caution is suggested for the high-yield segment.

- Among the sectors presenting the most interesting investment opportunities for the next quarter, the one related to animal needs stands out, namely food, veterinary diagnostics, and the pharmaceutical sector. The Pet sector has recorded extraordinary growth, exceeding 200 billion USD globally in 2023, with a forecast of further expansion in the future.

THE RISK FACTORS TO MONITOR:

- the return of inflation

- the slowdown in the US labour market

- recessions in various countries

- the geopolitical context (Israel-Palestine-Iran war, Russia-Ukraine and tensions in Taiwan) that could lead to rising oil price

.jpg)

2024 is about to end with a rise in the main American index, the S&P 500, by more than 25%, which puts it among the best years ever.

Analysing what led to such a strong rise, one discovers that only 12 percentage points derive from the growth in profits (the growth of cash is only 4%), while as many as 14 percentage points (at 2 December 2024) are due to the expansion in multiples. The P/E 2024 grew to 25 times, well above the historical average of 16. To be fair, consensus earnings growth for 2025 is 13%, which would bring P/E 2025 to 22 times.

This expansion of multiples was not driven by a fall in ten-year rates, to which valuations are linked, but by flows increasingly directed towards the American market, amplifying the premium at which it trades compared to the rest of the world and, in particular, Europe and China. Flows to the US stock market are at their highest in the last 12 years.

Quarterly flows to US equity funds and ETFs ($bn)

Source: Goldman Sachs International

Looking ahead to 2025, one cannot help but be cautious due to valuations and sentiment at its highest on the world’s main stock exchange. The US index represents almost 70% of the Morgan Stanley World index, although US GDP accounts for 26% of global GDP. In the following graph you can see how the risk premium of investing in American equities has been reduced to zero.

S&P 500 Equity Risk Premium (bp)

Source: Morgan Stanley

When valuations are so tight, it’s reasonable to expect low annual nominal average returns for the next ten years, say around 4%. Let’s not forget that, with the second Trump presidency, the risk of a strong internal clash in the country, in addition to the likely tensions with the rest of the world, will greatly increase the volatility and uncertainty about economic growth.

The increasingly pervasive presence of artificial intelligence will play a positive role in all product sectors. The problem is that to date 50% of the money invested in artificial intelligence comes from the five largest American companies, with the risk of a sudden slowdown in the event of a setback by the “Magnificent 7”. These amazing companies, with the Trump presidency, might not have an easy life: some members of the future administration are in fact strongly opposed to the domination of the large technology platforms.

If, on the other hand, we look at the real economy, the US economy continues to grow above 2%, despite the fact that two- and ten-year rates remain above 4%, driven by the positive wealth effect (strong rise in the stock market and real estate) and the re-shoring of production.

The big question mark for 2025 concerns the effect of the probable increase in import tariffs that Trump will impose on the rest of the world.

The growth of global trade over the past 50 years has contributed to 40% of the economic growth, making it plausible that any wars could slow down the global growth. On the other hand, the expected corporate tax cuts will support earnings growth and the increase in the deficit will be covered by higher revenues from tariffs.

Higher tariffs could cause inflation to rise slightly which, combined with a probable increase in the deficit, may prevent Fed funds from falling significantly. We estimate these could reach the 3/3.5% area by the end of 2025.

Equity markets outside the US trade at very reasonable valuations, but 2025 earnings could be negatively impacted by sharp increases in American tariffs.

.jpg)

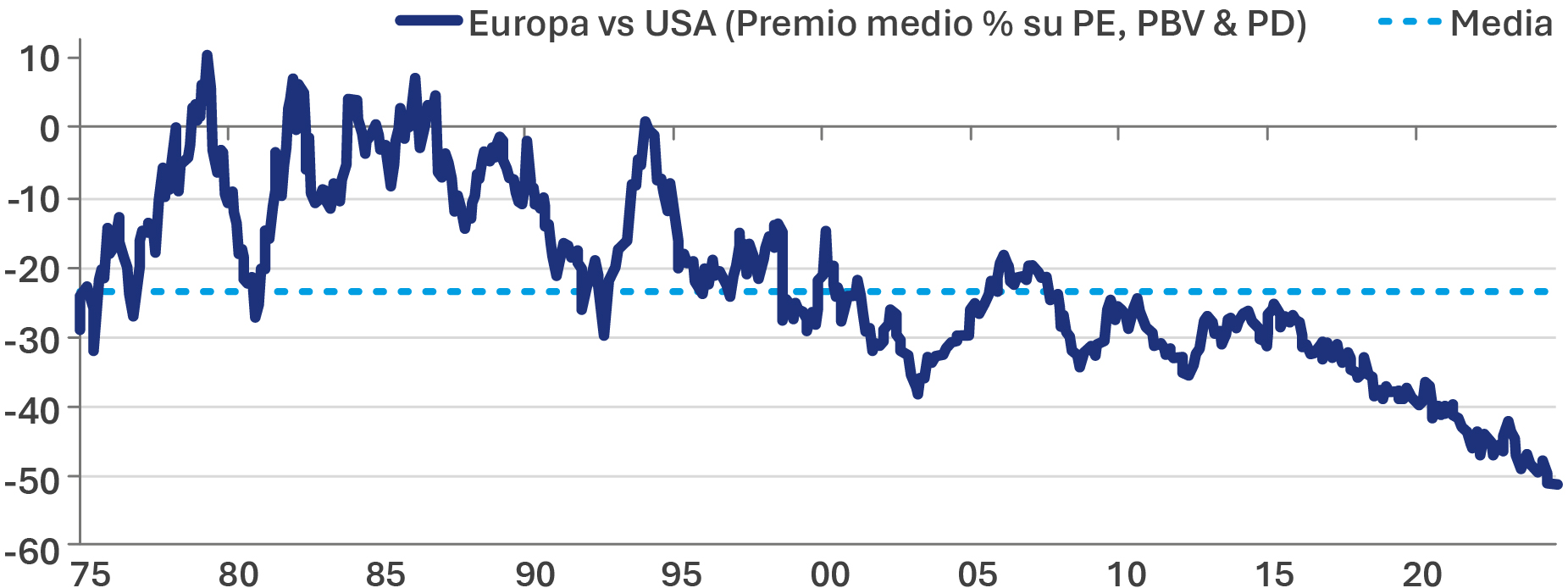

The following two graphs show that global investors’ positioning in Europe is at a 10-year low, despite valuations being at a 50% discount to US equities. This level of undervaluation has never been seen in the past 50 years.

Global positioning in euro area equity funds

Source: Goldman Sachs International

Average Europe vs USA valuation premium

Sources: MSCI, IBES, Morgan Stanley Research. Note: Average relative ratings use 12-month forward data, if available (forward P/E data starts in 1987), and trailing data if forward P/E is not available. Data as of October 31, 2024.

Europe is at a particularly critical moment, caught between a paralysing system of governance and some industrial policy errors. However, thanks to the weakness of the euro and the fall in interest rates, European equities are expected to end the year on a positive note.

In addition to geopolitical risk, Europe is paying a sharp increase in the price of energy, having lost the competitive advantage of Russian gas which flowed abundantly, especially to Germany. Europe found other alternative sources of gas supply, but the average price paid is much higher than the price paid by households and businesses in America, China and India.

On top of this we have weaker Chinese demand than in the past, the crisis of such an important sector as the automotive industry and excessive regulation that is often an obstacle to business. In Europe, the anti-trust regulator has blocked many mergers and acquisitions between European companies over the past decade. This is because they tend to look at the local market and not at the global market, with the result that we run out of European champions able to compete on a global scale.

The hope is that, after finally having the new European Commission in place, Europe will move quickly, in line with what is envisaged by the Draghi agenda on competitiveness. Europe must push towards the creation of leaders in digital technology and energy transition, as well as strengthening the more traditional sectors that are under threat on the one hand by US tariffs and on the other by Chinese competition and some Emerging countries. To do this, it will be necessary to mobilise large sums of money that only a single capital market can guarantee. And on this point the move of Unicredit which is trying to acquire a major German bank and MFE’s move on ProSieben, bode well.

It should be crucial for Europe, at a time when the future of trading with the USA is uncertain, to reach an agreement with Mercosur (Brazil, Argentina, Chile, Peru, Uruguay, Paraguay, Bolivia and Colombia), a market of 750 million people. Years ago a similar agreement was reached with Canada and the effects were extremely favourable for both parties. With regard to China, on the subject of tariffs, Europe is currently using a velvet glove so as not to jeopardise exports to the Asian giant.

European equity markets, especially in the small/mid-cap segment, are very undervalued both in absolute value and compared to similar American companies.

Clearly, the fall in interest rates that should materialise during 2025, as European inflation returns to the 2% area, should help flows to this segment of the market. The icing on the cake for European markets would be the end of the war between Russia and Ukraine.

In Italy, flows to the small/mid-cap segment are expected to improve significantly. In the first quarter of 2025 closed-end funds with a focus on small-mid cap companies, financed by the CDP together with domestic managers, will become operational. There are rumours of an allocation of about 1 billion euros with an expected life of at least six to seven years.

The weakness of the euro, which is expected to continue at the beginning of the next year, will certainly boost the profits of European exporters.

Looking East, the strong undervaluation of the Chinese market is striking. China is suffering from weak domestic consumption due to the continuing real estate crisis. The weight of the Chinese stock market is equal to 3% of the Morgan Stanley World index, despite China’s GDP representing about 20% of the world’s GDP.

In recent years, the Chinese government has impacted the equity markets several times, suddenly intervening in some sectors and causing significant losses to investors. For this reason and the political tensions with China, which indirectly supports Russia and continues to threaten Taiwan, global investors are very cautious about investing in the stock market of the Asian giant. Despite this, Chinese companies are increasingly competitive both domestically and in foreign markets, with exports to emerging countries that have now surpassed those towards the West.

The Chinese government has given various signals in recent months that it wants to support the stock market and domestic demand: it is very likely that over the course of the next year, China will increase its stimulus measures to the economy, especially if US tariffs were to curb its exports.

We believe that in the next decade, China will be able to impose its currency as an alternative to the US dollar on many countries – especially in Asia, Africa and Latin America – reversing a major competitive burden towards the US. China is therefore managing the exchange rate of the renminbi so as not to increase the value of public debt excessively. This is also very sustainable thanks to 10-year interest rates in the 2% area compared to 4.3% in the United States.

For this reason, we believe that a position, albeit moderate, in the Chinese stock market should be built with a medium-term perspective.

Against other currencies, the dollar is expected to remain strong with the exception of the Japanese yen where, after 30 years of deflation, Japan has returned to having an inflation rate above 2%. The Bank of Japan will therefore continue with a slow and steady rise in rates.

After two years of synchronised rate hikes around the world to counter the inflationary shock of 2022, monetary policy has finally reached its objective: to stabilise the inflation rate and pave the way for a gradual move to lower rates. However, the trajectory of this descent appears less linear than initially forecasted, highlighting a growing disconnect – or decoupling – between Europe and the United States.

In Europe, we are facing sluggish growth, aggravated by a crisis not so much cyclical as structural, which affects Germany and France. The ECB has started cutting rates with an initially cautious approach, but it is now forced to adopt a more assertive strategy. The recovery, awaited for 2025, seems increasingly distant. On the opposite front, the Fed faces a diametrically different situation. The US economy proves to be surprisingly robust and the new economic policy envisaged by the Trump administration could encourage a further acceleration, with accompanying inflationary pressures. In the United States, therefore, the fall in rates seems destined to be more limited than in Europe.

Despite the fact that US Treasuries offer a clear yield advantage over German Bunds, European bonds will likely be protected by a more accommodative monetary policy in 2025, with the ECB potentially cutting rates more frequently than the Fed.

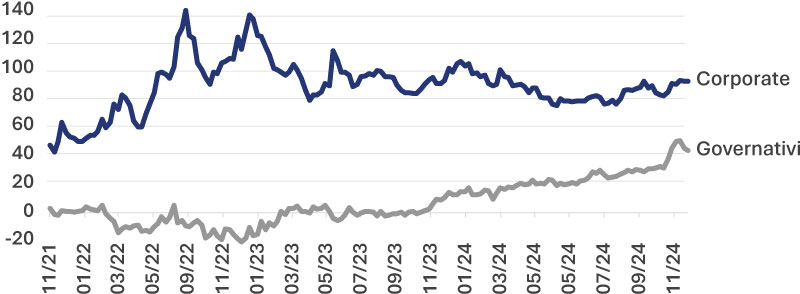

The credit market continues to outperform government bonds. Although economic growth remains disappointing, it is still positive, with a contained default rate. Investment flows continue to drive this asset class. Among the factors behind the reduction of spreads between corporate bonds and government bonds, a new element is emerging this year: the underperformance of government bonds.

In the chart, we look at the returns of European corporate and government bonds, both compared to swap rates. We can see a moderate compression of corporate spreads and a marked widening of government spreads. It is not only corporate outperformance, but also a clear underperformance of government bonds.

Spread vs. Swap Curve

Source: Banor calculations based on Bloomberg data

In Europe, as in the United States, government yields have progressively exceeded swap rates (monetary policy forecasts). This phenomenon is linked to the increase in government issuance, including in traditionally virtuous countries such as Germany. Although the market does not expect a default by the governments in Berlin or Washington, it is signalling that the growing issuance volumes are becoming increasingly heavy on bank balance sheets.

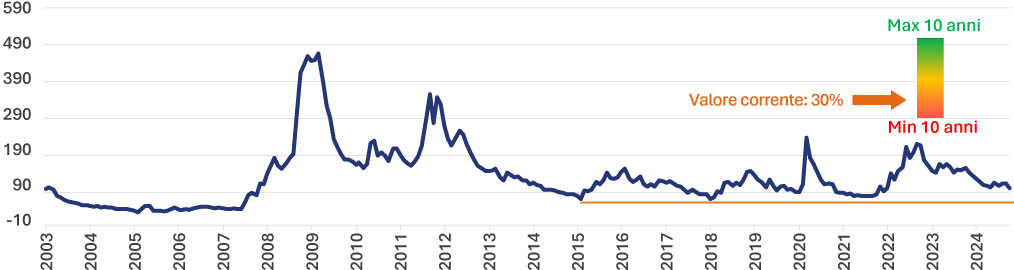

The underperformance of government bonds affects corporate bond valuations: comparing the spread versus German Bunds, we are in the lower part of the historical distribution of the last ten years (30th percentile), an area that we could define as “marginally expensive”.

Spread vs Bund

Spread vs swap

Source: Banor calculations based on Bloomberg data

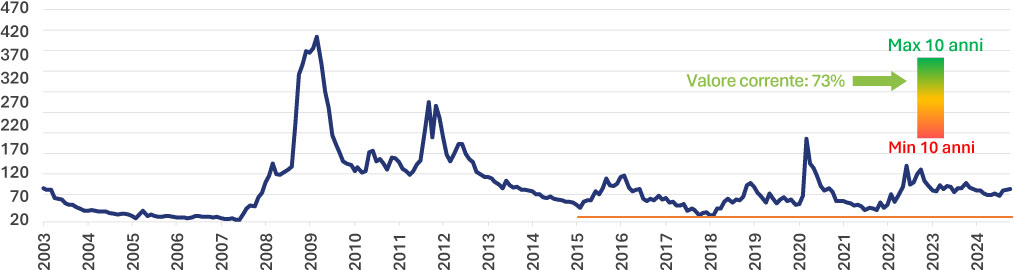

However, using swap rates as a reference – eliminating the effect of government underperformance – spreads appear significantly more attractive, standing at the 73rd percentile of the last decade.

These considerations lead us to maintain a preference for corporate credit, even after the excellent performance of the last year. Although in 2025, it will be more difficult to replicate the gains recorded since November 2023, returns remain good and above inflation. In addition, they will benefit from the support of an expansionary monetary policy and a macroeconomic environment that, although disappointing in Europe, should not result in a recession. In the absence of external shocks (possible but difficult to anticipate), credit tends to perform well in these scenarios, even with spread levels that are not particularly attractive and potentially for extended periods. This is the scenario we saw for three years between 2004 and 2007 (and between ‘94 and ‘97 in the US).

However, we are more cautious on high yield, given rising rates of default in recent months, which put the most indebted issuers at risk. To optimise portfolio returns, we prefer to overweight subordinated issues, both of banking issuers (Lower Tier 2, Tier 1) and industrial securities (the so-called “hybrid” securities). These instruments, typically issued by large, low-risk companies, offer a risk premium linked more to their complexity than to their real risk of default. These are ideal opportunities for a professional investment approach, based on the in-depth analysis of issuers and specific securities.

BETWEEN QUALITY FOOD, INNOVATIVE DIAGNOSTICS AND DRUGS

In recent years, the global pet care market has accelerated markedly, exceeding 200 billion dollars globally in 2023, with growth forecast at a rate of 6-7% per year between 2024 and 2032.

This growth reflects multiple supporting trends, such as rising interest rates – especially evident during the lockdown period linked to Covid – the “humanisation” of pets and the increase in their life expectancy, which today reaches 10-15 years for dogs and 15-20 years for cats.

The number of households with pets has grown globally, passing from 50% of households in 2010 to almost 70% in many developed countries in 2023. Suffice it to say that in the USA, 91 million households have a dog or a cat, more than double the 42 million with children under the age of 25.

In Italy, on the other hand, citizens spend about 950 million euros a year on the support of their pets, compared with 630 million intended for children.

Owners increasingly consider their pets as real family members, raising awareness about their health and driving demand for high-quality products and services. This phenomenon has produced a new sector of goods and services parallel to those destined to humans that is reflected in the in the key segments of pet food, veterinary diagnostics and pharmaceutical sector.

PET FOOD

The Pet food market – which today accounts for over 120 billion dollars globally – is constantly changing with increasing attention to premium and customised products. First of all, the sector is trying to respond to the changes in the preferences of consumers, creating functional food lines designed to improve digestive health, skin and coat or to meet specific needs related to breeds or life stages of animals. This is a winning strategy above all in emerging markets such as Asia and Latin America, where the middle class spending on pets is increasing.

Then there are those who produce fresh and natural food for animals, distributed through dedicated refrigerators in major supermarkets. The promise of a healthier and human-like diet is gaining support, particularly among younger owners who are attentive to the health of their pets.

However, the model presents some challenges: the necessary cold chain to keep products fresh involves high operating costs, which affect profitability. Despite this, the fresh pet food segment is one of the fastest growing markets, with even more potential largely unexplored.

VETERINARY DIAGNOSIS

If Pet food is the heart of daily care, diagnostics is the brain of the sector, promoting prevention and management of diseases. The market is worth about 8 billion dollars and has rates of growth close to double-digit.

Some companies have focused on technological innovation to respond to the needs of veterinarians and pet owners with products that range from diagnostic analysers to laboratory and software services for clinical management. This segment, which recorded a significant increase in revenues, reflects the willingness of owners to invest in the health of their pets, so as to prevent diseases, rather than treat them later.

VETERINARY DRUGS

Then there is the veterinary drugs sector, a segment often neglected in general economic discussions, but which represents a fundamental component for animal welfare and is worth about 45 billion dollars. We can consider drugs as the backbone of animal health, ensuring effective treatments for a wide spectrum of diseases, ranging from vaccines to dermatological drugs and pesticides, aimed at both pets and farms.

The veterinary drugs market recorded an average annual growth of 6% over the past decade, establishing itself as one of the most resilient sectors for investments due to its low correlation with the economic cycle. Statistical studies show that pet owners tend to keep the expense for their four-legged friends constant, even in the presence of a reduction in personal income of up to 20%.

Despite the opportunities, the pet sector faces some challenges, including rising inflationary pressure – which could affect consumers’ spending power – and rising operating costs for companies. For example – after the post-Covid boom – in the United States there has been a reduction in visits to veterinary clinics for several quarters. A further challenge for the sector is the risk of reputational damage deriving from the malfunction of a product or drug. Despite these challenges, the market remains resilient, with demand continuing to grow even in difficult economic environments.

The information and opinions contained herein do not constitute an invitation to conclude a contract for the provision of investment services, nor a personalised recommendation, are not contractual in nature, they are not drafted in accordance with a legislative provision and are not sufficient to make an investment decision. The information and data are believed to be correct, complete and accurate. However, Banor does not release representations or warranties, express or implied, as to the accuracy, completeness or correctness of the data and information and, where these have been processed or are derived from third parties, assume no liability for the accuracy, completeness, correctness or adequacy of such data and information, although it uses sources that it believes to be reliable.

The data, information and opinions, unless otherwise indicated, are to be considered updated at the date of writing, and may be subject to change without notice or subsequent communication. Any citations, summaries or reproductions of information, data and opinions provided herein by Banor must not alter their original meaning, may not be used for commercial purposes and must cite the source (Banor SIM S.p.A.) and the website web www.banor.it. The quotation, reproduction and in any case the use of data and information from third-party sources must take place, if permitted, in full compliance with the rights of the relevant owners.

Banor SIM S.p.A., with registered office at Via Dante 15 – 20123 Milan, registered in the Milan Companies Register no. 06130120154 – R.E.A. no. 1073114. Authorized by Consob resolution no. 11761 of 22/12/1998. Enrolled in the Register of Italian Investment Firms (SIM) at no. 31 and member of the National Compensation Fund (Fondo Nazionale di Garanzia).