Commentary by Angelo Meda, Head of Equities at Banor

Oil & gas: The Energy Question Between Geopolitics and Markets

Inflation above 2%? A highly unlikely scenario.

Let’s start with an important premise: given how fluid the situation is, it is impossible to have a clear view on the conflict in Iran. However, it is worth considering the impact it is having on the energy sector and, consequently, on inflation and interest‑rate dynamics.

The first argument often made by those monitoring oil prices is that rising crude prices will push inflation higher, forcing the ECB and the Fed to reconsider monetary policy. This has already been reflected in rate expectations: in Europe, the market has moved within a week from pricing a rate cut to pricing a hike by June. In the United States, expectations for the number of rate cuts in 2026 have decreased.

We do not believe central banks will change monetary policy—at least not because of this inflation spike. This is an external shock that does not justify “slamming the brakes” on the economy. The oil market will likely rebalance on its own without requiring policymakers to intervene to suppress demand.

It is helpful, however, to look more closely at the differences between oil and gas dynamics.

For more than 20 years the oil sector has experienced extreme swings—from $140 per barrel in 2008 to negative prices in 2020—with the physical market far less volatile than the financial one (financial markets trade over 100 times the amount of crude consumed each day).

First, it is essential to distinguish two separate factors: Iranian and Gulf oil production, and a potential blockade of the Strait of Hormuz.

Iranian production can be offset by higher supply from OPEC, the United States and, in a few months, Venezuela. There is therefore no real shortage risk. About 20% of global oil transits through the Strait of Hormuz, and it primarily serves Asia.

The consequence is that any price spike caused by a blockade would mainly affect short‑dated oil prices. Oil futures are priced on multiple maturities, and the curve reflects this.

One of the key indicators used by physical‑market operators is the spread between the short‑term price (one‑month maturity) and the medium‑term price (3–6 months). Today, the one‑month vs. six‑month spread shows a significant discrepancy.

Why?

Expectations for inventories. When there is risk of a physical shortage, demand for immediate delivery jumps and so does the price—exactly what happened after Russia’s invasion of Ukraine in 2022. The opposite occurs when there is oversupply (e.g., 2020 during Covid, the 2010 demand drop, or OPEC’s overproduction in 2015).

In normal conditions, this spread should be around $2–4, reflecting storage costs. Today, it is $16.4, similar to levels seen during the Russia–Ukraine war.

Conclusion: the crude market is already pricing physical‑market stress—stress that historically tends to fade quickly (within weeks or a couple of months at most).

This will have an effect on inflation, which will likely show a temporary spike due to energy prices, but it should last only a few months.

More broadly, the economy is increasingly less energy‑intensive: the shift from industrial to service‑based economies means that producing one unit of GDP today requires roughly half the energy needed in the 1960s.

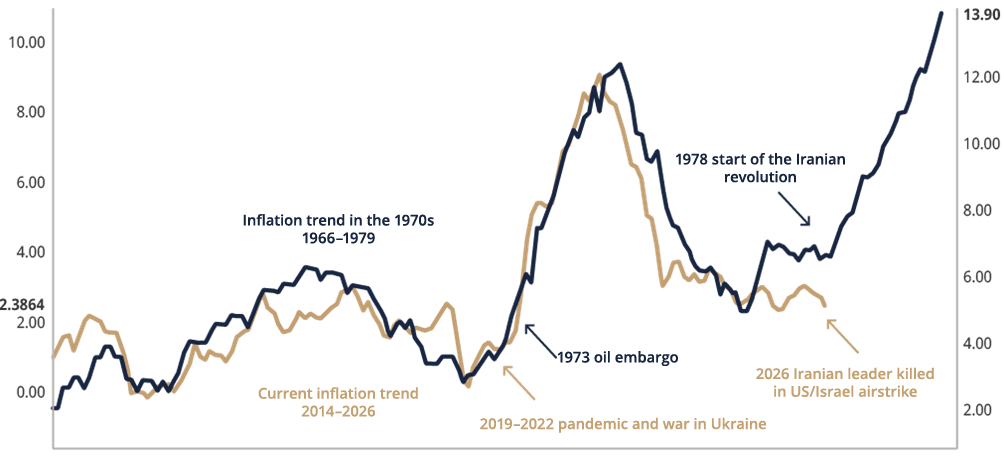

INFLATION: PARALLELS WITH THE 1970S?

Source: Bloomberg

Those who believe history repeats itself may see similarities between inflation in 1966–1979 and the past 12 years: A stable inflation cycle before the 1973 oil embargo (Yom Kippur War, Suez Canal closure); A sharp rise, followed by a decline; And a second shock driven by the 1978–79 Iranian Revolution. This leads some to expect a resurgence in inflation—not to 1979–80 levels, but high enough to force central banks to shift policy.

In this context, monitoring the natural gas and electricity markets is more important than monitoring oil. The energy mix has changed dramatically in the last 50 years: gas and electricity now account for 25–28% of global energy consumption vs. 56% in the 1970s. After the oil crises, hydro and nuclear grew significantly, and technological developments in extraction have made natural gas much more available (whereas it was previously burned off—flaring—during oil extraction).

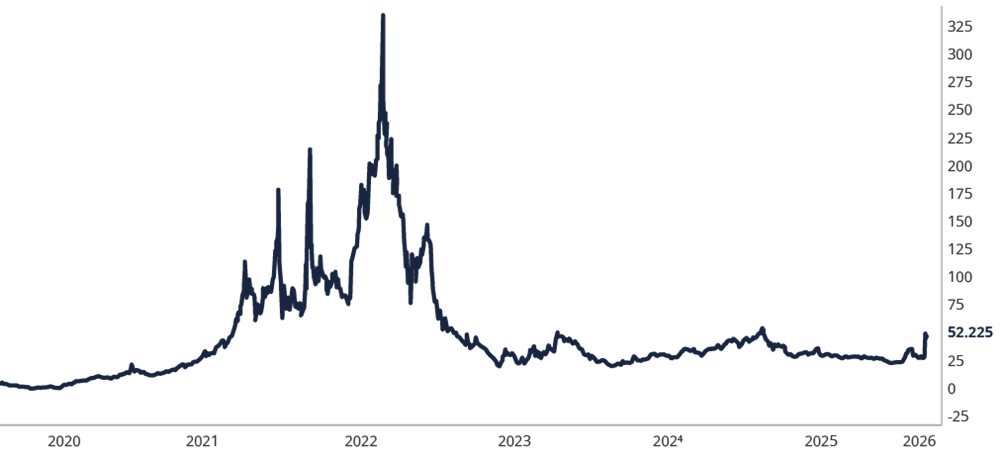

Turning to gas: gas prices determine the marginal price of electricity in Europe after liberalisation. In recent weeks gas prices have risen, but nowhere near the surge seen in 2021 after Russia’s invasion of Ukraine.

ONE MONTH TTF GAS PRICE WITH DELIVERY AT THE AMSTERDAM HUB

Source: Bloomberg

It may therefore be more important to track gas prices than oil prices.

However, one risk should not be underestimated: storage levels are low, close to 2022 levels. A slightly colder winter and stable supply conditions reduced the incentive to accumulate gas ahead of the second half of the year. Companies remain optimistic about supply capacity, and exports from Qatar and other major producers are expected to resume soon. Still, this is a variable worth monitoring: a rush to secure LNG—especially from the U.S.—could push prices to levels that are more problematic for the economy.

Overall Assessment.

Looking at the broader energy picture, we believe the inflation impact is limited and largely confined to the coming months. The recent move in interest rates appears poorly justified. At present, it is hard to imagine inflation staying permanently above 2% in a way that would force the ECB to intervene.

How should we interpret the market moves of recent weeks?

As a normal adjustment after a strong rally, driven mainly by excessively optimistic positioning. Historically, during wartime episodes:

- Equities typically fall 6–8%

- Oil often rises

- The dollar strengthens

- Bonds, gold and other currencies show mixed reactions

The removal of Maduro in January and a brief conflict involving Iran could lead to higher oil production in the second half of the year, potentially acting as a catalyst for lower inflation and rate cuts—coinciding with the U.S. mid‑term elections in November.

It is difficult at this stage to take a definitive position, as everything depends on the duration of the Iran–Israel/Gulf conflict. But in our view, markets have priced in a very unlikely scenario. Historically, such geopolitical episodes generate market moves that require careful risk assessment but also create attractive investment opportunities for those who understand the dynamics and can take informed positions.

The information and opinions contained herein do not constitute an invitation to take out a contract for the provision of investment services, nor a personalised recommendation; they are not contractual in nature, they are not drafted pursuant to a legislative provision, and they are not sufficient to make an investment decision. The information and data are deemed to be correct, complete and accurate. However, Banor does not issue any representation or guarantee, express or implied, on the accuracy, completeness or correctness of the data and information and, where these have been prepared by or derive from third parties, does not assume any liability for the accuracy, completeness or adequacy of such data and information, even if its sources are deemed to be reliable.

Unless indicated otherwise, the data, information and opinions are understood to be up-to-date at the date of preparation, and may change without notice or subsequent communication. Any citations, summaries or reproductions of the information, data and opinions provided herein by Banor should not alter their original meaning, nor may they be used for commercial purposes, and they must cite the source (Banor SIM S.p.A.) and the website www.banor.it. Citation, reproduction and use in any case of data and information from third-party sources must, if permitted, fully comply with the rights of the related data controllers.

Banor SIM S.p.A., via Dante 15 – 20123 Milan, registered in the Business Register of Milan 06130120154 – R.E.A. (Economic and Administrative Index) of Milan 1073114. Consob authorisation, resolution no. 11761 of 22/12/1998. Registered in the Register of Brokerage Companies (SIM) under no. 31 and member of the Italian National Guarantee Fund (Fondo Nazionale di Garanzia).